Private Foundations Gave $2.6 Billion in Grants to National Donor-Advised Funds in 2021

Last year, we analyzed the tax returns of electronically-filing private foundations and found that, in total, they had given nearly one billion dollars in grants to national donor-advised funds in 2018. That was the most recent data we could get at the time.

This May, the IRS released an avalanche of long-awaited nonprofit tax filings, so we are now able to update our findings through 2021. We found $2.6 billion in grants going from private foundations to donor-advised funds at national sponsors in 2021 alone.

Private foundations are currently allowed to make grants to donor-advised funds, or DAFs, and to count those grants toward their charitable distribution requirement of 5 percent of their assets each year. As we detailed in our report Warehousing Wealth, DAFs are giving vehicles with little transparency and no payout requirement at all, so this should be concerning to any taxpayer who wants to ensure that the charitable revenue they subsidize moves out to working charities in a timely manner.

This is especially important in the case of commercial DAFs like Fidelity Charitable Gift Fund and Schwab Charitable where the sponsors have a significant financial interest in donations staying put, generating management fees for their affiliated financial institutions.

The DAF granting we found prior to 2020 is almost certainly an undercount, since we only examined giving from private foundations to national DAFs — not DAFs held at community foundations or other nonprofit organizations. And we were only able to analyze the foundations that filed their taxes online — not the ones that filed on paper.

Thanks to a new reporting requirement, however, all foundation tax returns are required to be filed electronically starting in 2020. This means that the grants we found represent about 65 percent of all foundation filings up through 2019, and closer to 95 percent of the foundation filings in 2020 and 2021. And the $2.6 billion going from foundations to national DAFs in 2021 is, by itself, a huge amount of charitable revenue cycling between bank accounts.

Other Key Findings about Foundation-to-DAF Giving

Using the data newly published by the IRS, we identified tax returns for 127,330 private non-operating foundations that filed electronically in at least one year from 2017 to 2021. 3,577 of these electronic filers gave to a national DAF in at least one of these five years. Unless otherwise specified, the findings below are based on these 3,577 electronically-filing, national-DAF-giving foundations.

- Private foundation giving to national DAFs averaged $1.4 billion per year from 2017 to 2021. This giving has been increasing rapidly; foundations gave more than $2.6 billion to national DAFs in 2021 alone.

- When private foundations give to national DAFs, their grants to those national DAFs are much larger than their gifts to other recipients. From 2017 to 2021, gifts from DAF-giving private foundations to national DAFs averaged just over $682,000 each, while their gifts to other recipients averaged just over $88,000 each.

- 713 foundations gave $1 million or more to national DAFs from 2017 to 2021. 138 of these foundations gave $10 million or more to national DAFs over these five years.

- For 167 foundations, grants to national DAFs made up one hundred percent of qualifying charitable distributions — the amount used to evaluate whether the foundation has met its minimum payout requirement for the year. For another 477 foundations, national DAF giving made up 90 to 99 percent of their qualifying charitable distributions over those five years.

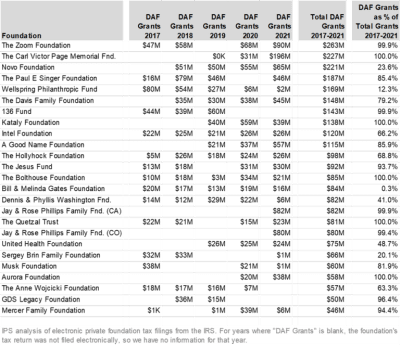

Top 25 National-DAF-Giving Foundations

Several of the largest DAF donors—the Zoom Foundation, the 136 Fund, the Quetzal Trust, and the Hollyhock foundation—also appeared in our earlier 2021 analysis, as well as in reporting on the topic by the Chronicle of Philanthropy. For many of the foundations on the list, DAF grants made up all or nearly all of their charitable distributions over these five years.

Top 10 National DAF Recipients

Foundation gifts to commercial DAFs were not evenly distributed: Fidelity Charitable received

the lion’s share, with the National Philanthropic Trust a fairly distant second.

What We Can Do

This sort of transfer shouldn’t count as charity. Donors get tax deductions for putting money into private foundations so that money can go to real charities. And the 5 percent payout requirement is meant to ensure that that happens. But when foundations use grants to donor-advised funds to meet payout, it subverts the public purpose behind that requirement.

The dollars flowing from private foundations to donor-advised funds make for a considerable amount of money delayed in reaching active charities. Foundation DAF giving, as well as DAF giving in general, has been on a steep upward trajectory, and as it grows it has been steadily eating into the revenue that has historically gone to working nonprofits.

Together foundations and donor-advised funds now take in 37 percent of all individual giving every year. The scale, growth, and nature of this kind of giving make it more important than ever to have improved DAF governance, as well as greater transparency into DAF giving.

For more information, and for what we can do to fix this, see our previous reporting on this at Inequality.org.