Four CEO Pay-Related Taxes in Play on Capitol Hill

Americans believe the ratio between CEO and worker pay should be no higher than 7 to 1, according to one academic survey. Last year, in the middle of a pandemic, average CEO pay ran hundreds of times greater than typical employee pay. At 58 U.S. corporations, the CEO-worker pay gap was more than 1,000 to 1.

Senate Democrats are looking at ways to address these disparities while also generating revenue for President Biden’s ambitious Build Back Better plans.

According to news reports, Senate Finance Committee Chair Ron Wyden has developed a list of about a dozen and a half revenue options. Four of these would deliver the additional benefit of curbing CEO pay.

CEO pay ratio tax

One of Wyden’s options is an excise tax on corporations with big gaps between CEO and worker pay. This is no doubt inspired by the Tax Excessive CEO Pay Act, a bill championed by Senators Bernie Sanders and Elizabeth Warren and Representatives Barbara Lee and Rashida Tlaib and supported by the AFL-CIO, the Center for American Progress, and numerous other organizations and academics.

Tax incentives to narrow pay disparities should appeal to Senator Joe Manchin and other moderate Dems. An overwhelming 86 percent of Americans believe CEOs make way too much money. This sentiment might be even stronger in Manchin’s West Virginia, where Big Pharma execs have made a fortune flooding poor communities with opioids.

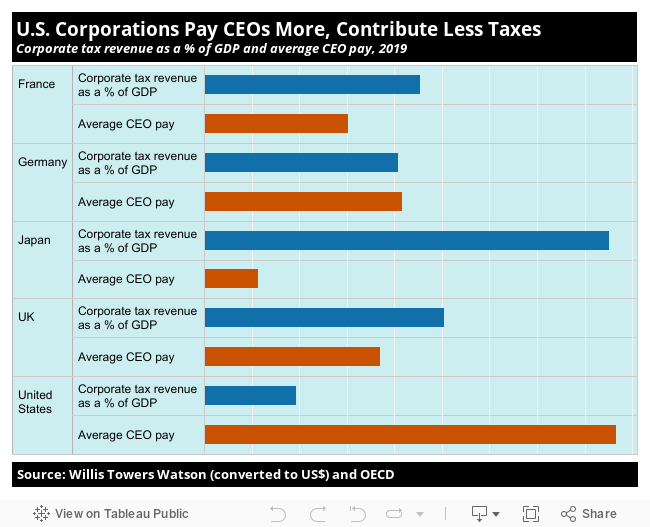

A CEO pay excise tax could also boost U.S. corporations’ global competitiveness. Opponents of raising the U.S. corporate tax rate often point to lower statutory rates in other large economies. But huge loopholes in the U.S. tax code have lowered the effective rate that corporations actually pay the IRS. While U.S. corporate tax revenue as a share of GDP is lower than in any other G7 country, average American CEO pay is off the charts.

Chief executives at big U.S. corporations make eight times as much on average as their counterparts in Japan, three times as much as in France, and twice as much as in the U.K. and Germany. Using tax policy to incentivize more rational U.S. CEO pay levels could improve business competitiveness, since study after study shows that exceptionally high CEO pay correlates with mediocre financial performance.

Extensive resources on CEO pay ratio taxes, including municipal-level precedents in Portland and San Francisco, are available on the Institute for Policy Studies web site Inequality.org.

Buybacks tax

Wyden’s revenue list reportedly includes another excise tax that could curb CEO pay — a levy on companies that repurchase a “significant” amount of stock.

As Professor William Lazonick and other analysts have long documented, stock buybacks artificially inflate executives’ stock-based pay and siphon off capital that could be used for productive investment. As one academic put it, buybacks motivate executives “to game their incentive compensation arrangements and turn them from pay for performance into pay for manipulation.”

In the first year after the 2017 Republican tax cuts, S&P 500 firms spent a record $806 billion on share repurchases. With growing cash reserves at many corporations and big banks, analysts are now predicting a buyback resurgence.

Republican Senator Marco Rubio was the first to float a legislative proposal for taxing buybacks in 2019. Wyden and fellow Democratic Senator Sherrod Brown will reportedly issue their own plan this week.

Carried interest loophole

On the campaign trail in 2016, President Donald Trump called for the closure of a loophole that gives wealthy private equity, real estate, and hedge fund managers a huge tax break by allowing them to pay the discounted capital-gains tax rate on so-called “carried interest” (earnings tied to a percentage of the fund’s profits). This income actually amounts to compensation for managing other people’s investments and should be taxed as ordinary income. Republicans made only modest changes in the treatment of carried interest in their 2017 tax reform.

Wyden has introduced a bill to treat carried interest as ordinary income, as has been proposed by the Biden administration, Senators Tammy Baldwin, Elizabeth Warren, and others. However, Wyden’s approach would go further by requiring managers to pay an annual tax on accrued carried interest, based on an assumed rate of return on assets, regardless of whether or not the managers realized gains. The proposal would raise an estimated $63 billion over a decade.

The U.S. Chamber of Commerce made preposterous claims this week that Wyden’s proposal would result in the loss of nearly five million U.S. jobs and even insinuated that if such a reform had been in place, we wouldn’t have a Covid vaccine. Leading carried interest expert Professor Victor Fleischer quickly shredded what he calls the Chamber’s “bogus study.”

Bonus deductibility cap

Another option on Wyden’s list would “expand restrictions on business deductions for employees making more than $1 million.” This should also have trans-partisan appeal, since it builds on a provision in the Republicans’ Tax Cuts and Jobs Act.

While that 2017 legislation mostly cut taxes for the rich and big corporations, one section actually made a small step forward on CEO pay reform. Since 1993, corporations had enjoyed a huge loophole that allowed them to deduct unlimited amounts of executive pay off their taxable income — as long as that pay was in stock options or other forms of so-called “performance” pay. In other words, the more corporations paid their CEO, the less they owed in taxes.

The 2017 tax reform partially closed the loophole by setting a $1 million deductibility cap on all compensation going to a corporation’s CEO, CFO, and three other highest-paid employees. The 2021 American Rescue and Recovery Act took another step forward by closing the loophole for compensation going to an additional five executives (10 in total).

Democratic Senators Jack Reed and Richard Blumenthal and Rep. Lloyd Doggett have proposed extending the $1 million deductibility cap to all forms of compensation for all employees in their Stop Subsidizing Multimillion Dollar Corporate Bonuses Act.

The public investment proposals on the table in the budget reconciliation negotiations, from universal child care to free college, would dramatically reduce our nation’s staggeringly high levels of inequality. Paying for them with tax reforms that tackle key inequality drivers — including runaway CEO pay — would move us even further down the path towards an equitable society.

Originally in Inequality.org.