Democrats’ Budget Deal Will Collect Billions from the Wealthy to Invest in Human Needs

Democrats appear to be finally closing in on a legislative agreement to enact President Biden’s Build Back Better plan.

After months of obstruction from conservative Democratic Senators Joe Manchin and Kyrsten Sinema, the WhiteHouse framework announced on Thursday is far less ambitious than the president’s original proposal. But the compromise nevertheless represents a long-overdue rejection of the failed “trickle down” theories the wealthy and their advocates in Congress have used to justify economic policies that benefit the rich at the expense of the rest of us.

Finally, after decades of Congress catering to the interests of those at the top, the Build Back Better plan will collect nearly $2 trillion from the wealthy and big corporations to invest in children, seniors, and workers.

The plan will expand access to affordable health care, child care, and home care, establish universal pre-k, create millions of new clean energy jobs, impose penalty fees on union-busters, and more. Advocates also beat back Manchin’s demands to impose work requirements and other restrictions on the expanded Child Tax Credit, which will increase economic security for 35 million families.

On the tax side, the plan includes several path-breaking reforms to raise more revenue from those who can afford to pay — the wealthy and large, profitable corporations.

We are particularly encouraged by a surtax on the annual gross income (including capital gains) of mega-millionaires and billionaires that is very similar to a proposal the Institute for Policy Studies and other fair tax advocates have been pushing for the past two years. The Build Back Better model applies a 5 percent surtax on income above $10 million and an additional 3 percent surtax on income above $25 million. This is expected to raise $230 billion over a decade from around 22,000 of the richest U.S. households.

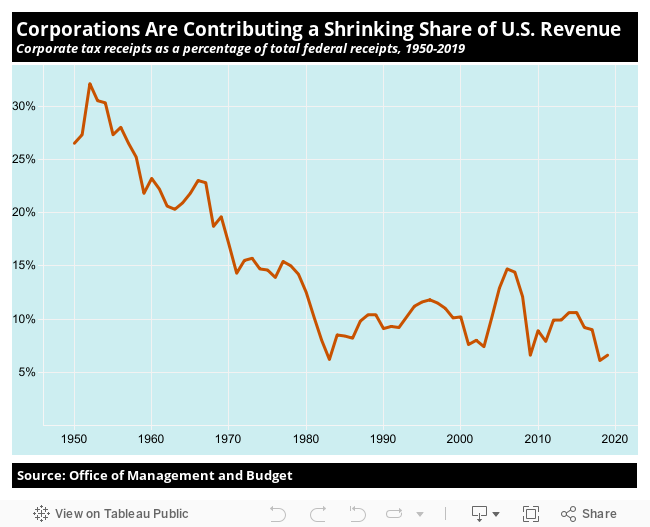

The deal also introduces minimum effective tax rates of 15 percent on large U.S. corporations’ domestic and foreign profits. This will bring the United States in line with a recently inked, 136-country agreement aimed at discouraging offshore tax dodging. And hopefully these changes will reverse a decades-long trend of corporations contributing a shrinking share of federal revenue. That share plummeted from 32.1 percent in 1952 to 6.6 percent in 2019.

In another historic first, the deal will introduce a 1 percent surcharge on corporate stock buybacks, a maneuver that diverts resources that could be used for R&D or wage increases and artificially inflates CEOs’ stock-based pay. As one academic put it, buybacks motivate executives “to game their incentive compensation arrangements and turn them from pay for performance into pay for manipulation.”

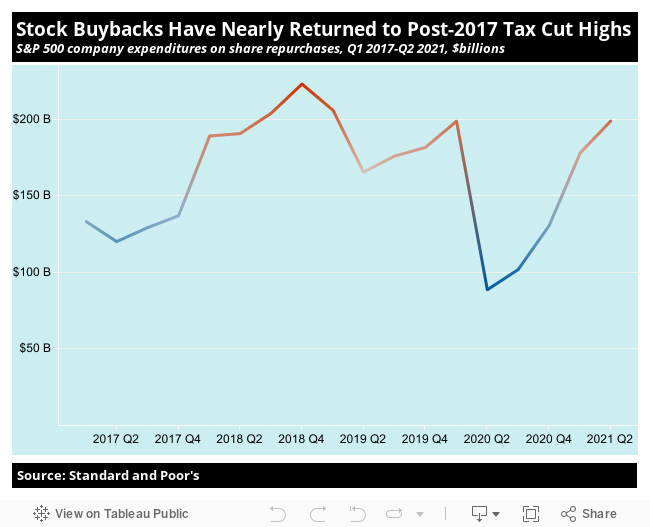

S&P 500 firms blew nearly $200 billion on stock buybacks in the second quarter of this year — approaching the records set in the period after the 2017 corporate tax cuts. The new tax will discourage this wasteful use of corporate resources.

The deal also provides funding for beefed-up IRS enforcement that will make it much harder for the ultra-rich to cheat on their taxes. But we are disappointed that Manchin, Sinema, and other conservative Democrats blocked key proposals for tackling wealth inequality.

Senate Finance Chair Ron Wyden had pushed, with President Biden’s support, a “Billionaires Income Tax” that would’ve required the 1,000 or so richest U.S. households to pay annual taxes on the increased value of their investments, whether or not they sold the underlying assets. This would’ve addressed flaws in our current tax code that allow the ultra-rich to pay lower average tax rates than most teachers and firefighters.

The billionaires tax proposal lost momentum after Manchin said he found it divisive to target this particular group — despite the fact that U.S. billionaires have increased their fortunes by $2.1 trillion during a pandemic that has cost millions of lives and livelihoods.

Other proposals to address our country’s extreme wealth concentration also wound up on the cutting room floor, including estate tax fixes and the closure of the “stepped-up basis” loophole that allows the ultra-rich to avoid capital gains taxes on assets they pass on to their heirs.

Democrats also failed to find consensus on other inequality-fighting tax reforms, including Wyden’s proposals to close the carried interest loophole that benefits private equity and hedge fund managers and to impose an excise tax on excessive CEO pay.

From the get-go, Congressional Progressive Caucus Chair Pramila Jayapal has described the Build Back Better plan as a “down payment” on the bold, transformational agenda Americans need. Members of her caucus are expected to vote for the deal, even as they — and most progressive activists — acknowledge that much more needs to be done to achieve a fair tax system and an equitable economy.

The ideological shift represented by this agreement should make it easier to secure future victories.

“The supply-side, trickle-down spell has finally been broken,” said Frank Clemente, head of the Americans for Tax Fairness coalition. “President Biden’s Build Back Better framework recasts the debate and blazes the trail for further progress.”

Originally in Inequality.org.